Why Property Insurance Rates Continue to Rise in Louisiana.

Louisiana property insurance rates spiked by 4.4% in 2025, resulting in a $135 million increase for policyholders statewide. Louisiana policyholders already pay the second-highest rates in the nation, at more than $3,800 above the national average.

Why are property insurance rates continuing to climb in Louisiana? Because state regulators are ignoring the real problem. They are regulating the people of Louisiana, not the insurance industry.

After Hurricanes Laura and Ida, 11 insurance companies collapsed — forcing stranded storm victims to go to court to recover what they were owed.

Why did these companies go insolvent? Before the storms, those companies moved hundreds of millions of dollars off the books to unregulated affiliates, where they purchased executive perks like a $5.7 million hunting lodge. Their greed came first. Policyholders were an afterthought.

While that was the most egregious behavior, other insurers routinely delayed and denied claims, sending victims through a maze of adjusters and paperwork. According to a 2022 survey by LSU, roughly half of all Louisiana residents were dissatisfied with how insurance companies handled property damage claims.

Instead of demanding accountability from bad-faith insurers, Commissioner Temple has blamed storm victims at every turn.

- In a recent interview, Commissioner Temple chose to victim-blame Louisiana families. He said catastrophe-related litigation was a key driver in rising home insurance premiums, ignoring that the spike in litigation following the storms was due to bad-faith insurers failing to handle claims properly.

- In 2024, Temple declined to punish 17 shady insurers that generated an unusually high volume of complaints from policyholders after Hurricane Ida.

- Temple’s legislative packages have all focused on regulating the people of Louisiana by stripping away their legal rights, rather than the industry he was elected to regulate on their behalf.

Commissioner Temple’s approach to Louisiana’s insurance crisis has made it harder for storm victims to file claims and easier for insurance companies to delay and deny claims, or cancel policies.

- Home insurers operating in Louisiana denied 44.6% of claims filed in 2024, according to Weiss Ratings.

- According to a recent poll, 85% of respondents say Louisiana’s insurance market is “poor” or “very poor.” Another survey shows that two-thirds of respondents saw a premium increase, roughly 50% struggled to find coverage, and approximately 1 in 10 reported having their policy cancelled by their insurer.

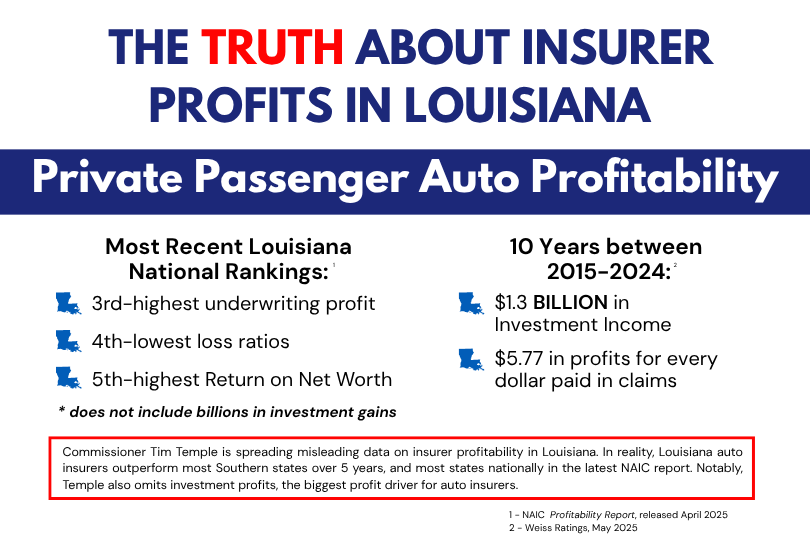

- Meanwhile, home insurers operating in Louisiana have invested your premium dollars to the tune of $88.3 billion and reported just $1.6 billion in underwriting losses, meaning they made $55 in profit for every dollar they lost.

As a former insurance executive, Temple sees Louisiana’s insurance crisis through the lens of the insurance industry. Temple is blind to the plight of Louisiana policyholders. With the legislative session upon us, Louisiana policyholders need the legislature to step forward and pass common-sense laws that hold insurers accountable, strengthen consumer protections, and lower rates.